Mortgage and Market Insights

- Alisa Aragon-Lloyd

- Dec 12, 2025

- 4 min read

Markets are moving again: What the latest numbers mean for you

Canada’s latest economic releases sparked quite a reaction first from analysts, then from bond markets, and now from lenders. On the surface, the headlines looked bright: a surge in employment and a sharp rebound in GDP. But a closer look tells a more complicated story.

What is really behind the jobs and GDP Jump

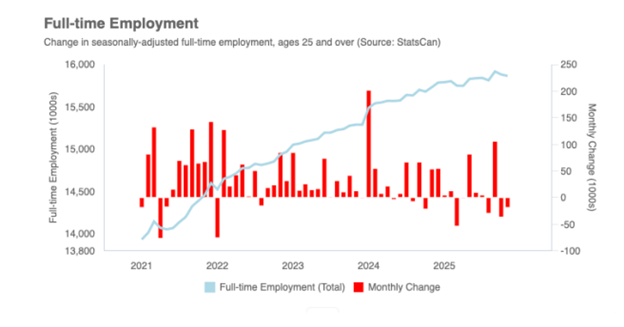

The numbers came in far stronger than expected:

Employment was expected to drop by 5,000 jobs, instead it jumped by 53,600.

GDP was forecast at -0.5%, and instead delivered +2.6% annualized growth for Q3 2025.

But when we dig deeper, the picture changes:

93% of new jobs came from the 15–24 age group, mostly part-time likely tied to pre-holiday hiring.

Full-time employment for those 25+ fell by 18,000, a more meaningful economic indicator.

GDP growth was driven largely by government spending and a sharp drop in imports, not by broad economic strength.

Household consumption fell for the first time (outside of the pandemic) in nearly 20 years, and business investment slipped.

This softer undercurrent is why many economists are urging caution even as the headline numbers look optimistic.

How the bond market reacted

While GDP didn’t move markets much, the jobs report certainly did.

The bond market jumped 0.20% in a single day, the sharpest move upward in more than three years. Within hours, lenders began increasing fixed mortgage rates.

In moments where the data feels misleading or overly rosy, the bond market tends to be the clearest signal. And the signal right now is this:

We may have reached the short-term bottom for fixed mortgage rates.

If you are planning to buy in 2026, or have a renewal next year, it may be wise to secure a rate hold just in case this indeed proves to be the floor.

Some lenders will allow you to break your mortgage within 120 days of renewal without penalty, which can create real opportunities for those with higher-rate mortgages from two or three years ago.

Rate Update: What’s next for borrowers?

Variable/ Adjustable Rates

We may have seen the final cut of this cycle. Going into the last announcement, markets were pricing only a 5% chance of another reduction, the lowest probability of all year.

Why do traders think this may be the end (for now):

Inflation is still above the target

Unemployment dropped sharply due to last week’s job gains

GDP bounced back above expectations

It’s a trio of data points pointing in the wrong direction for anyone hoping for lower variable rates.

Could more cuts still happen? Yes, in an “outside chance” scenario. But there’s also a risk inflation re-accelerates, pulling variable rates upward again.

Fixed Rates

Fixed rates continue to be the roller coaster of the mortgage world. Unexpected data swings markets harder than ever, and this month’s job report delivered the biggest upward jump in bonds in more than three years.

The general forecast remains:

Fixed rates will likely trend slowly higher over time.

That’s why a 5-year fixed is looking attractive again, especially for borrowers wanting stability.

Considering locking in your variable?

With the recent spike in bonds, now may be a strategic time to lock in, especially if you were already thinking about it. If this isn’t the absolute low point, it’s likely very close to it. The only major risk factor that could push rates lower again is a collapse of the CUSMA (Canada-United States-Mexico Agreement) trade agreement in January, which could send Canada’s economy into a tailspin.

Final thoughts: fixed or variable?

With the latest shift in forecasts, the 5-year fixed now slightly edges out the 3-year fixed, followed by variable. But here’s the important nuance:

If your priority is near-term payment relief, a variable may still be more attractive, depending on your situation.

As always, the right mortgage strategy isn’t just about the rate you get today; it’s about aligning your financing with your plans, your risk tolerance, and your long-term goals.

Industry Update: Consolidation, credit unions & the future of lending

2025 has been a watershed year for consolidation in BC’s credit union sector. Several major mergers are reshaping the lending landscape:

Coast Capital, Prospera, and Sunshine Coast Credit Union voted to merge, creating Canada’s largest national credit union by 2026.

Vancity and First Credit Union are merging (effective Dec 1).

Coastal Community and Integris have entered merger discussions.

Beem Credit Union continues rapid expansion after absorbing G+F Financial, Blueshore, and more.

What this means for borrowers?

There are clear pros and cons:

Pros of consolidation:

Better technology

More competitive products

Broader reach (especially if moving between provinces)

Cons:

If a credit union becomes federally regulated, underwriting becomes stricter

Provincial credit unions often offer more flexible policies, especially for rental income

There’s also a larger shift underway: AI will accelerate consolidation.

Large institutions will invest heavily in technology. Smaller ones may struggle to keep pace. Borrowers should expect the “big vs. small” divide in lending to widen over the next few years.

Want to plan ahead confidently?

Mortgages don’t have to be complicated. With the right guidance and strategy, the process can be clear, calm, and straightforward.

Comments